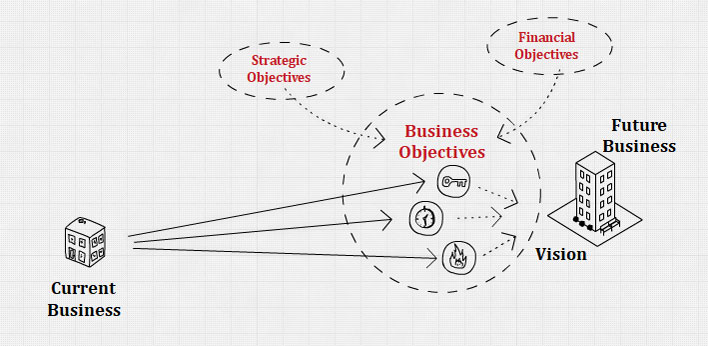

Business Objectives

What is a Business Objective?

Business objectives are specific results that an organization seeks to achieve in pursuing its mission and vision.

The objectives of a business are the end results of planned activity. The achievement of objectives should result in the fulfillment of the mission and vision statement. This can be thought of as what society is giving back to the organization as it does the work of fulfilling its mission and vision.

Business objectives represent the results expected from pursuing certain strategies. Strategies represent the actions to be taken to accomplish long-term objectives. The time frame for objectives and strategies should be consistent, usually from two to five years.

Business objectives should be quantitative, measurable, realistic, understandable, challenging, hierarchical, obtainable, and congruent among organizational units. Each objective should also be associated with a timeline.

Objectives are commonly stated in terms such as growth in assets, growth in sales, profitability, market share, degree and nature of diversification, degree, and nature of vertical integration, earnings per share, and social responsibility.

Clearly established objectives offer many benefits. They provide direction, allow synergy, aid in evaluation, establish priorities, reduce uncertainty, minimize conflicts, stimulate exertion, and aid in both the allocation of resources and the design of jobs.

Objectives provide a basis for consistent decision-making by managers whose values and attitudes differ. Objectives serve as standards by which individuals, groups, departments, divisions, and entire organizations can be evaluated.

Business objectives are essential for organizational success because they state direction, aid in evaluation, create synergy, reveal priorities, focus coordination, and provide a basis for effective planning, organizing, motivating, and controlling activities.

In a multidimensional firm, business objectives should be established for the overall company and for each division.

Long-term objectives are needed at the corporate, divisional, and functional levels of an organization. They are an important measure of managerial performance. Without long-term objectives, an organization would drift aimlessly toward some unknown end. It is hard to imagine an organization or individual being successful without clear objectives. Success only rarely occurs by accident; rather, it is the result of hard work directed toward achieving certain objectives.

Types of Objectives

Two types of objectives are especially common in organizations: financial and strategic objectives.

Financial objectives include those associated with growth in revenues, growth in earnings, higher dividends, larger profit margins, greater return on investment, higher earnings per share, a rising stock price, improved cash flow, and so on.

Strategic objectives include things such as a larger market share, quicker on-time delivery than rivals, shorter design-to-market times than rivals, lower costs than rivals, higher product quality than rivals, wider geographic coverage than rivals, achieving technological leadership, consistently getting new or improved products to market ahead of rivals, and so on.

Although financial objectives are especially important in firms, oftentimes there is a trade-off between financial and strategic objectives such that crucial decisions must be made.

The dangers associated with trading off long-term strategic objectives with near-term bottom-line performance are especially severe if competitors relentlessly pursue increased market share at the expense of short-term profitability.

And there are other trade-offs between financial and strategic objectives, related to riskiness of actions, concern for business ethics, need to preserve the natural environment, and social responsibility issues.

Both financial and strategic objectives should include both annual and long-term performance targets.

Ultimately, the best way to sustain competitive advantage over the long run is to relentlessly pursue strategic objectives that strengthen a firm’s business position over rivals. Financial objectives can best be met by focusing first and foremost on the achievement of strategic objectives that improve a firm’s competitiveness and market strength.

Methods to Avoid

Management should avoid the following methods for setting objectives.

The first method is setting objectives by extrapolation.

This is the idea to keep on doing about the same things in the same ways because things are going well.

The second method is setting objectives for the crisis.

This is based on the belief that the true measure of good management is the ability to solve problems that occur every day. Managing by crisis is a form of reacting rather than acting and of letting events dictate what and when to make decisions.

The third method is setting objectives by subjective.

This is built on the idea that there is no general plan for which way to go and what to do; just do the best you can to accomplish what you think should be done.

The fourth method is setting objectives by hope.

This is because the future is laden with great uncertainty and that if we try and fail, then we hope our second (or third) attempt will succeed. Decisions are predicated on the hope that they will work, and the good times are just around the corner.

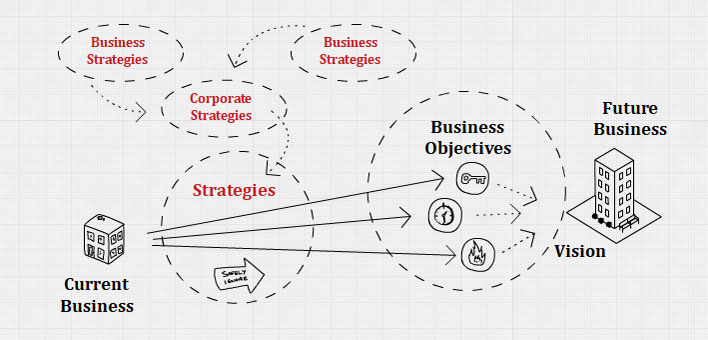

Strategies

What is a Strategy?

Strategies are comprehensive plans that state how the organization will achieve its mission and objectives. It maximizes competitive advantage and minimizes competitive disadvantage.

Strategies are potential actions that require top management decisions and large amounts of the firms’ resources. In addition, strategies affect an organization’s long-term prosperity, typically for at least five years.

Strategies have multifunctional or multidivisional consequences and require consideration of both the external and internal factors facing the firm.

Strategy Types

There are usually 3 types of strategy and they form a hierarchy of strategy within an organization.

They are: (1) corporate strategy, which describes the company overall direction and attitude toward growth; (2) business strategy, which occurs at business unit or product level, and emphasizes improvement of the competitive position of the products and services of the company within the selected industry or market segment; and (3) functional strategy, which describes how each function achieve corporate and business unit strategy by creating and maintaining distinctive competences.

Strategy making is not just a task for top executives. Middle and lower-level managers too must be involved in the strategic planning process to the extent possible.

In large firms, the persons primarily responsible for having effective strategies at the various levels include the CEO at the corporate level; the president or executive vice president at the business level; and the respective chief finance officer (CFO), chief information officer (CIO), human resource manager (HRM), chief marketing officer (CMO), and so on, at the functional level.

In small firms, the persons primarily responsible for having effective strategies at the various levels include the business owner or president at the company level and then the same range of persons at the lower two levels, as with a large firm.

It is important to note that all persons responsible for strategic planning at the various levels ideally participate and understand the strategies at the other organizational levels.

This practice helps ensure coordination, facilitation, and commitment while avoiding inconsistency, inefficiency, and miscommunication.

Plant managers, for example, need to understand and be supportive of the overall corporate strategic plan (game plan) while the president and the CEO need to be knowledgeable of strategies being employed in various sales territories and manufacturing plants.

Many, if not most, organizations simultaneously pursue a combination of two or more strategies, but a combination strategy can be exceptionally risky if carried too far.

No organization can afford to pursue all the strategies that might benefit the firm. Difficult decisions must be made. Priority must be established. Organizations, like individuals, have limited resources. Both organizations and individuals must choose among alternative strategies and avoid excessive indebtedness.

Strategy Initiation

Strategy formulation is typically not a regular, continuous process. Humans tend to continue a particular course of action until something goes wrong or a person is forced to question his or her actions.

This period of strategic drift may result from inertia, or it may reflect the belief of management that the current strategy is still appropriate and needs only some fine-tuning. This phenomenon, called punctuated equilibrium, describes corporations as evolving through relatively long periods of stability (equilibrium periods) punctuated by relatively short bursts of a fundamental change (revolutionary periods).

Some sort of shock to the system is needed to motivate management to seriously reassess the situation of the organization. This triggering event can be (1) having a new CEO, (2) having an external intervention, (3) facing a threat of change in ownership, (4) having a performance gap, or (5) having a strategic inflection point.

Approaches to making Strategic Decisions

Strategic decisions are decisions that deal with the long-run future of an organization.

It has the 3 following characteristics: (1) Rare – strategic decisions are unusual and typically have no precedent to follow, (2) Consequential – strategic decisions commit sustainable resources and demand a great deal of commitment from the organization, and (3) Directive – strategic decisions set precedents for lesser decisions and future actions throughout the organization.

As organizations grow larger and more complex, with more uncertain environments, decisions become increasingly complicated to make. One of the distinguishing characteristics of strategic management is its emphasis on strategic decision-making.

In pursuit of such objectives, one will find themselves on a quest to follow a certain strategic decision-making framework. The following are the 4 most common approaches to strategic decision making.

Approach 1: Entrepreneurial Mode

Strategy decisions are made by one powerful individual. This type of decision usually focuses on opportunities; problems are secondary. Strategy is guided by the vision of the founder. The goal is about the growth of the organization.

Approach 2: Adaptive Mode

Strategy decisions that focus on reacting solutions to existing problems, rather than a proactive search for new opportunities. Strategy is made to move the corporation forward incrementally.

Approach 3: Planning Mode

Strategy decisions involve a systematic gathering of appropriate information for situation analysis, generation of feasible alternative strategies, and the rational selection of the most appropriate strategy. This planning mode includes both the proactive search for new opportunities and the reactive solution of existing problems.

Approach 4: Logical Incrementalism

Strategy decisions that combine planning, adaptive, and entrepreneurial modes. In this type of strategic decision-making, top management has quite a clear view of the mission and objectives of the organization. However, the actual strategy is allowed to emerge out of the debate, discussion, and experimentation. This approach can be useful when the external environment is changing quickly, or consensus and commitment within the internal environment are critical.

Process of making Strategic Decisions

The following are the 8 fundamental steps to the strategic decision-making process.

Step 1: Evaluate current performance results, in terms of (1) financial goals and (2) current mission, objectives, strategies, and policies.

Step 2: Review corporate governance, which is the performance of the board of directors and top management.

Step 3: Scan and assess the external environment to determine the strategic factors that pose Opportunities and Threats.

Step 4: Scan and assess the internal corporate environment to determine the strategic factors that are Strengths and Weaknesses.

Step 5: Analyze strategic factors (SWOT analysis) to pinpoint problem areas and review mission and objectives, if necessary.

Step 6: Generate, evaluate, and select the best alternative strategy in light of the analysis conducted previously.

Step 7: Implement selected strategies using programs, budgets, and procedures.

Step 8: Evaluate implemented strategies via activities of evaluation and control.

Resources

Further Reading

- How to Write Business Objectives? (indeed.com)

- Objectives of Business (economicsdiscussion.net)

- Business Objectives (cio-wiki.org)

- Demystifying Strategy: The What, Who, How, and Why (hbr.org)

- What The Heck Is A Strategy Anyway? (forbes.com)

- What Is Strategy (and Why Should You Care)? (braintraffic.com)

Related Concepts

References

- Hitt, M. A., Ireland, D. R., & Hoskisson, R. E. (2016). Strategic Management: Concepts: Competitiveness and Globalization (12th ed.). Cengage Learning.

- Hitt, M. A., Ireland, D. R., & Hoskisson, R. E. (2019). Strategic Management: Concepts and Cases: Competitiveness and Globalization (MindTap Course List) (13th ed.). Cengage Learning.